The 4 Pillars of Investment and Trading Success

1. Understanding macro, micro and market fundamentals

If you are going to play the game, you need to understand the rules. Now, I’d be the first to admit that the rules are not always clear and they seem to be changing all the time, but this is the nature of dynamic complex systems and you certainly need a starting point to work from. If you don’t understand what drives markets, then you don’t have much of a chance to succeed in investing. The following is an extract from an article I wrote during the bear market of 2022 which details my approach to market fundamentals:

“Some investors and traders look at the market with only one lens, such as valuation or technical price structure, but I believe that it is better to look through multiple lenses to build sufficient confidence in your strategy. The problem with this multi-lens strategy is, well, “analysis paralysis”. If your analysis is confusing and prevents you from making clear decisions, it defeats the purpose. Therefore, it is imperative that you have a well-defined framework for forming a view on markets which feeds into your investment strategy. My simplified model of what drives markets will be the focus of this article.

I have categorized the market drivers into 6 broad categories, in no particular order. All are important but difficult to rank or weight in terms of impact. Markets are vastly complex systems and the framework described below tries to simplify the complexity into an easily comprehensible model, which means it is fallible. “All models are wrong, some are useful” (Prof George Box). I find this one useful in the sense that it frees me from the dreaded “analysis paralysis”, and it has worked for me (so far anyway).”Follow the link below to read the article:

Nov 3, 2022

Bear on its Back? (Part I)

What drives the stock-market anyway?

2. Understanding market psychology and price action

In his book “The Alchemy of Finance” (A compulsory read for all investors and traders) George Soros provides a compelling framework for understanding market dynamics. Reflexivity, as described by Soros, posits that market participants’ perceptions, biases and actions can influence market fundamentals, which in turn, affect market participants’ perceptions and actions. This feedback-loop between market participants and market fundamentals can lead to self-reinforcing cycles that drive markets away from equilibrium, creating the well-known boom-bust cycles observed in markets.

Reflexivity challenges the traditional economic theory that markets tend towards equilibrium (Efficient Market Hypothesis) and that market participants act rationally, basing their decisions solely on available information. Instead, Soros argues that markets are often driven by the perceptions and misconceptions of participants, who are influenced by their own biases and the actions of others. This can lead to periods of irrational exuberance or undue pessimism, causing asset prices to deviate significantly from their underlying fundamentals. In addition to Reflexivity, the uneven distribution of the ability of market participants to imagine the unknown also flies in the face of the Efficient Market Hypothesis.

This is what makes predicting markets near impossible and why it is crucial to understand the psychological cycles that drive group behavior. In addition to “The Alchemy of Finance”, “Mastering the Market Cycle” by Howard Marks is an excellent book that deals with market psychology.

Used in isolation, I find price chart analysis highly inadequate for decision-making. However, it remains the simplest method to gauge the dominance of fear, greed, euphoria, panic, doubt, or despair in the collective psyche of the market. It is very effective in identifying levels of support and resistance where, if breached, the market’s perception of, and bias towards the traded asset has shifted.

3. Mastering your own psychology and how it relates to market psychology.

“You can’t manage your money if you can’t manage your emotions” ( Warren Buffett)

Apart from understanding market psychology, you have to be aware of your own biases as well — and not just be aware of them but be able to guard against being influenced by them in your analysis and resultant investment decisions. It is in this process where most investors/traders fail. It requires deep introspection and brutal honest self-criticism — a process most humans find near impossible for many psychological reasons.

The above is also one of my motivations for publishing this website and my Medium articles. If I cannot write a logical argument for my decisions, then I’m probably being swindled by my own biases. I also hope to provoke constructive criticism from readers to point out potential mistakes or biases in my reasoning.

4. Strategy and execution.

Strategy and Execution: This pillar focuses on integrating the insights from the aforementioned three pillars into a cohesive methodology and process aimed at generating returns within a disciplined framework of risk management and systematic decision-making processes.

Influential works like Jack Schwager’s Market Wizards series, Beating the Market by Edward Thorpe, and Agustin Lebron’s The Laws of Trading have been instrumental in shaping my investment approach and procedures.

For me, the most important aspect to consider is ensuring that the chosen methodology and strategies align well with your objectives, timeframes, and, ultimately, your personal inclinations and style. Afterall, solving the market is very hard work and if you’re not going to enjoy the process, you are unlikely to succeed.

For more details on my methodology and process, click the link below.

The Problem of Induction

Why explanations are important and why historical data can be misleading – Knowing what you don’t know.

Turkeys and the Problem of Induction

Induction, as a method of gaining knowledge, says that a thesis can be derived directly from a set of observations. Then, when subsequent observations fall within the extrapolations of that thesis, the thesis is proven to be correct, without having to explain the causal link between the thesis and the observations.

A simple example illustrating the problem with this method, is the often quoted (and very apt) “Thanksgiving turkey”. It goes something like this:

A turkey who gets fed every day at the same time for three hundred days, using the method of induction, could conjecture that the farmer is a caring, turkey-loving person and that on the next day he will be fed again just as it was fed every day for as long as the turkey can remember. If the next day, the farmer feeds the turkey again, the turkey will feel that its thesis has held up and that it must therefore be true. For every subsequent day it gets fed, this belief will be strengthened. That is until the day before Thanksgiving. On this day, the turkey might see that the farmer is not approaching the pen with a bucket of feed, but instead, with a butcher’s knife. The inductivist turkey might explain this by saying, “I know what butcher’s knives are used for, but I have never observed that the farmer has used the knife on me in that way and therefore this new information is irrelevant to my thesis.” Needless to say, the turkey was going to get the surprise of its life, and not in a good way.

It is important to note that I do not exclude historical observations as part of the process of understanding the environment, on the contrary, observations are critical to test one’s theories. The problem arises when you induce your thesis directly from the observations and thereby skipping the critical step of coming up with good explanations of why the thesis led to those observations and therefore has a good probability (all else being equal) of leading to the same outcomes in the future.

At the risk of stepping on some toes, I think many (not all) technical analysts find themselves (unknowingly) ensnared in this problem of induction. I would include an earlier version of myself here. Nothing against TA — It is a powerful and useful tool within its applicable domain, as long as you stick to that domain, understand the problem of induction, and know how to avoid it.

Blindly relying on statistics without considering the effect that underlying economic and market fundamentals might have on the probability of the outcome, is reckless. Understanding the qualitative cause-effect relationships of the underlying drivers of the market says more about what might happen next than what history of what has happened, tells us.

This does not mean history is useless — no, history can tell us about those cause-effect relationships, but the data-points without good explanations can be misleading. As David Deutsch puts it: “The overwhelming majority of theories are rejected because they contain bad explanations (or no explanation at all), not because they fail experimental tests.”

So, if your back-test gives you 15 out of 15 positive results, without a good fundamental explanation of why those results were achieved, it is a worthless signal, or worse, no signal at all. Yes, it took the wise words of a physicist who has zero interest in markets to make me realize this truth.

Risk, Returns and Alpha

The very first fundamental mind shift I had to make at the beginning of my investing career was to think in terms of probabilities and alternative histories, rather than in deterministic outcomes which, with the right knowledge, can be predicted. This mindset lies at the heart of my investment philosophy.

Howard Marks beautifully describes the relationship between risk, returns, and alpha in his memo titled ‘Fewer Losers, or More Winners?’ I will paraphrase and quote some extracts from this memo, as I could not articulate it better myself, and will provide the link to the memo below.

Here is Howard Marks:

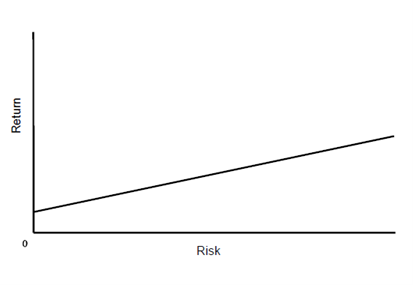

“When I attended graduate school at the University of Chicago 55 (!) years ago, I was taught to view the relationship between risk and return as follows:

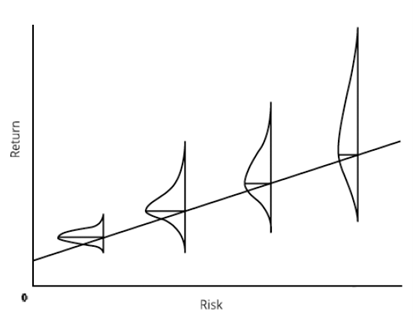

But the more I thought about it, the more unhappy I was with the way the linear presentation of the purported relationship tells investors that they can count on achieving higher returns as a result of taking more risk. After all, if that were really the case, risky investments wouldn’t be riskier. Thus, in my memo Risk (January 2006), I suggested a different way of depicting the relationship by superimposing on the line a series of bell-shaped probability distributions turned on their side:

Rather than implying that taking more risk – moving from left to right in the graph – assures higher returns, this new way of looking at the relationship suggests that as you take more risk, (a) the expected return increases, as per the original version above; (b) the range of possible outcomes becomes wider; and (c) the bad possibilities become worse. In other words, riskier investments introduce the potential for higher returns, but also the possibility of other less-desirable side effects. That’s why they’re described as being riskier.

The last element I want to touch on is what I call “alpha,” or individual investing skill. The reason the EMH (Efficient Market Hypothesis) disdains efforts to beat the market is its conviction that since securities are always priced correctly, the ability to identify bargains to buy and over-pricings to avoid can’t exist. Theory’s assertion that there’s no such thing as mastery of markets implies that no one has the skill to assemble portfolios that outperform. This is why I depict the bell-shaped curves above as symmetrical: In an efficient market, investors can only take what the market gives them.

But I’m convinced the potential to improve on that through skill does exist in some markets and some people. Investors who possess alpha have the ability to alter the shape of the distributions in the graphs above so that they’re not symmetrical, in that the portion of the distribution representing the less desirable outcomes is smaller than the portion representing the better ones. In fact, that’s what alpha really means: Investors with alpha can go into a market and, by applying their skill, access the upside potential offered in that market without taking on all the downside risk. In my memo What Really Matters? (November 2022), I said the key characteristic of superior investing is asymmetry – having more upside than downside. Alpha enables exceptional investors to modify the probability distributions such that they are biased toward the positive, resulting in superior risk-adjusted returns.”

To read Howard Marks’s memo, click below:

I believe that the ability to manufacture an asymmetrical return distribution where the downside risk is limited while the potential upside remains wide open (depicted in the chart above), is the primary goal of, and key to successful investing (or trading).