Background

In 2016, I constructed a multi-strategy hedge fund portfolio as my core long term investment strategy. At the time, I felt that years of Quantitative Easing and unsustainable debt levels in the global economy posed higher risks than was recognised by the traditional (long only) investment industry. I wanted exposure to the potential continued upside of markets, while also enjoying some protection against large drawdowns.

Today, with global debt on a seemingly exponential trajectory and financial markets growing ever more fragile, this approach has become even more important than in 2016. Soon after inception of the initial fund, friends and family started asking me to manage funds for them as well. I decided to create an investment vehicle in the form of an En Commandite Partnership (or LP) whereby funds could be pooled and managed alongside my personal core portfolio.

It is important to emphasize that this is a private fund and it is not available to the public as an investment product.

Fund Objective

The fund’s objective is to deliver superior returns, with reduced volatility, relative to the SA Multi-Asset Medium Equity Category Average (benchmark) over any 3-year rolling period. The fund aims to achieve this by:

- skilled active management,

- employing a wide range of financial instruments, including derivatives instruments and,

- by diversifying across asset classes, strategies and investment managers.

Portfolio Construction

“Diversification is the only free lunch in finance.” (Harry Markowitz)

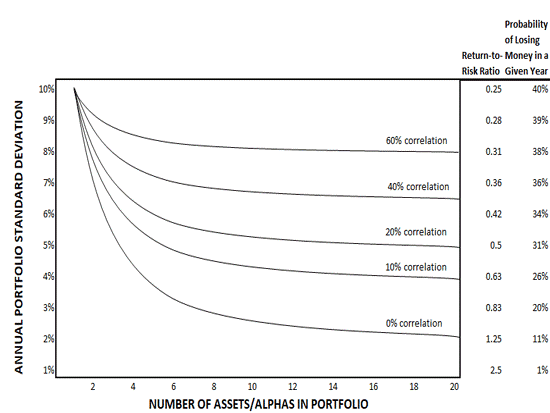

While this principle holds significant merit, its impact on portfolio performance has boundaries. Ray Dalio’s illustration, he dubbed “The Holy Grail of Investing,” sheds light on the dynamics between risk, return, correlation, and diversification, revealing that:

- The portfolio’s overall volatility diminishes with lower correlation among its assets (income streams), as shown by the lowest volatility curve (at the bottom of the chart) offering the highest return-to-risk ratio.

- The advantage of diversification notably declines after incorporating more than 15 assets (income streams), highlighting the diminishing returns of over-diversification.

- Portfolios with less than six diversified assets witness a rapid deterioration in their return-to-risk ratio, emphasizing the importance of a balanced diversification threshold.

In summary, the goal is to combine strategies that yield high returns, exhibit no (or low) correlation with each other, and demonstrate resilience to market shocks. This enhances the resilience of the entire portfolio, not only due to the low correlations but also thanks to the intrinsic characteristics of the individual strategies, which include the strategic use of derivatives and the implementation of stringent risk management protocols.

Currently, the most resilient strategy within our WRI portfolio is the Market Neutral approach, which spans across five asset classes, including commodities, on top of the conventional 4 (Stocks, Bonds, Property and Cash). Given the present market uncertainty, this strategy is prioritized in the fund, benefiting from its ability to withstand volatile market conditions through its comprehensive risk management and versatile use of derivatives.

Strategy descriptions

1. Market Neutral

This strategy invests in five asset classes – stocks, bonds, listed property, commodities and cash – and employs a market neutral approach.

In a simplified depiction, consider a Market Neutral strategy as taking positions in both strong and weak companies within the market. You might invest in the strongest companies (taking long positions) while simultaneously betting against the weakest companies (taking short positions). The aim is to balance these positions to achieve a net zero exposure to the overall market movements.

For instance, in a rising market, your investments in strong companies are expected to yield higher returns than the losses incurred from the short positions in weak companies. Conversely, in a declining market, the gains from shorting weak companies could surpass the losses from the long positions in strong companies. So, you make money irrespective of whether the market is going up or down – Magic! Well, if only. This is an oversimplification. In practice, the unpredictable nature of company performances and market dynamics like mean reversion (e.g. powerful rallies of weak stocks in a broader downtrend), can influence the strategy’s outcomes. Real-world application of a Market Neutral strategy involves detailed analysis and rigorous risk management to successfully navigate market complexities.

2. Fixed Income Derivatives Trading

In this strategy, the yield curve serves as a vital tool (See chart below). This curve plots bond yields against their respective maturities, offering crucial insights for making strategic decisions in fixes income derivatives investments. Traders analyze the curve’s shape to gauge shifts in the economic landscape and interest rate movements, aiming to spot pricing anomalies in the fixed income market. The objective is to capitalize on these anomalies by executing trades that will benefit from expected adjustments in the market. This approach not only aims to exploit these temporary mispricings for potential gains but also prepares traders to react when the market begins to realign with underlying economic indicators

3. Equity Long/Short Strategies:

The portfolio incorporates two distinct equity long/short strategies: one targeting global equity markets and the other focusing on the South African Equity market. These strategies are designed to identify undervalued stocks believed to appreciate in the future for long positions, and overvalued stocks expected to decline for short positions. Unlike Market Neutral strategies, which aim for neutral market exposure, these long/short strategies actively seek opportunities in both directions regardless of the net bias of the total strategy. The overall bias of this strategy, whether long or short, is determined by the prevailing market opportunities; if long opportunities outweigh short ones, the strategy will exhibit a long bias, and vice versa.

4. Crypto and Gold Strategy:

This is a long-only strategy that maintains exposure to a diversified portfolio of crypto assets, primarily Bitcoin, and gold mining companies. At first glance, combining these assets into one bucket might seem unconventional, but they share key characteristics: Both Bitcoin and Gold are scarce monetary assets with minimal to no counterparty risk. In an economic landscape marked by increasing deficit spending and the debasement of fiat currencies, I regard exposure to such assets as crucial. The preference for gold mining companies over the metal itself is strategic; miners tend to exhibit leveraged responses to gold price fluctuations, meaning their valuations can move more significantly than the price of gold itself. Moreover, while they are closely correlated with gold prices, gold miners offer the additional benefit of paying dividends, unlike the gold commodity, which does not produce any yields.

5. Exponential Technologies

This is also a buy and hold strategy where I focus on buying stocks of nascent technological industries where there could be explosive growth into the future. These industries include Robotics, Energy Storage, Artificial Intelligence, Biotech, Space Exploration and Synthetic Materials.

6. Cash

This is not really a strategy, but rather an allocation decision. I hold some cash in times where I think there might be exceptional opportunities ahead in any of the abovementioned strategies. In the current environment, where cash earns very attractive interest rates, I am inclined to hold a larger position than in the past.